Macro & Market Views

Cutting Through the Waves: Corporate Governance in Japan

Cutting Through the Waves: Corporate Governance in Japan

After decades of struggle, animal spirits in Japan seem to have reawakened in the post-Covid era, driven by both cyclical and secular forces.

- The continuation of stimulative policy as the rest of the developed world began to tighten helped revive Japanese equities in recent years. Even following this strong performance, however, Japanese market valuations currently remain below that of US indexes.

- As support from accommodative monetary and fiscal policy wanes, a sustained focus on improved corporate governance may provide a more durable underpinning to markets.

- Despite widespread dividend increases and share buybacks, corporate cash balances have continued to accumulate, suggesting substantial additional opportunity for companies to reward their shareholders.

- Ever cognizant of macroeconomic and geopolitical risks, we believe an eclectic group of well-run, well-priced Japanese companies may offer the potential to contribute to portfolio resilience.

Recovered Gross Domestic Product (GDP), healthy inflation and a weaker yen—along with improved governance practices—drove corporate profits and market indexes to new highs in local-currency terms earlier this year. Yet even following robust gains, valuations for Japanese equity markets currently remain muted relative to the US.

Although the Bank of Japan (BOJ) ended its yield-curve control and negative interest rate policies in March 2024—and increased its shortterm interest rate again in late July—monetary policy remains highly accommodative, and the road to normalization is fraught with risk. Meanwhile, at the fiscal level, the government has committed to achieving a primary budget surplus in a little over a year. But even as support from monetary and fiscal policies wanes over time, markedly improved corporate governance standards—including the return of capital to investors through dividends and buybacks—may provide a durable underpinning to Japanese equity markets.

Beyond cyclical and secular forces, broader macroeconomic and geopolitical considerations persist. Global financial markets are priced for only moderate levels of risk, and any perceived adverse development could trigger a swift and significant response—a dynamic we got a taste of in early August. That said, we believe bottom-up global stock picking underpins portfolio resilience—including in Japan, where we believe many high-quality, well-priced businesses may be found.

Revived Animal Spirits After Decades of Struggle

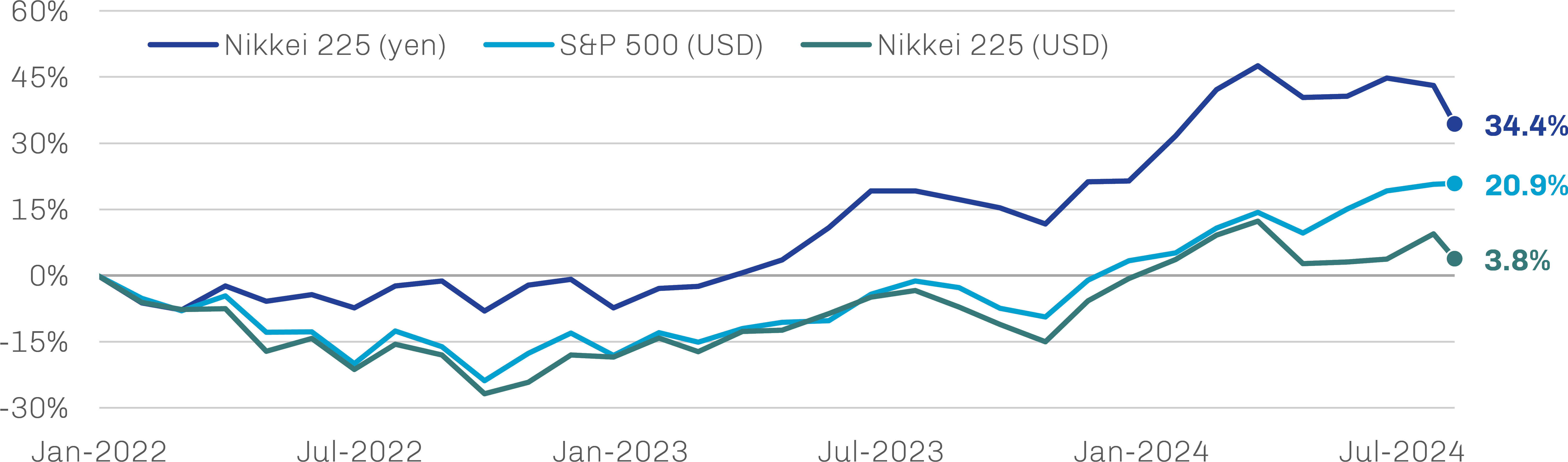

Following decades of sluggish economic growth, deflation and lagging investment returns, there have been signs in recent years that Japan may finally have regained its footing. Real GDP surpassed its pre-Covid peak in 2023 as healthy inflation took hold.1 At the same time, redirected capital flows out of China combined with aggressive monetary and fiscal stimulus—including both low real rates, which drove the yen to a generational low against the dollar and provided Japanese exports with a competitive leg up, as well as significant deficit spending—have underpinned equity markets. With surging corporate profits helping to rekindle animal spirits, the Nikkei 225 Index in February 2024 reclaimed its previous 1989 peak and subsequently set a series of new record highs before the early-August selloff. Notably, however, the benchmark’s 34.4% gain in local-currency terms over the past 32 months translates into a mere 3.8% when denominated in dollars; as shown in Exhibit 1, the S&P 500 Index is up 20.9% over the same period.2

Exhibit 1. Japanese Equities Are Riding High in Local-Currency Terms

Total Return, January 2022 through August 2024

Source: Bloomberg; data as of August 15, 2024.

Past performance is not indicative of future results.

Japanese equity markets were substantially undervalued throughout the post-global financial crisis period, in our view, and their relative valuation remains attractive despite their recent success. At 15.6 times earnings as of mid-August 2024, the MSCI Japan Index traded below its long-term average and at a significant discount to the S&P 500 Index’s multiple of 23.0.3

Even as Policy Tailwinds Fade...

The overall strength in Japanese equities since 2022 at least partially reflects a range of cyclical tailwinds, while recent volatility highlights the market’s sensitivity to policy changes. Having arguably achieved its goal of sustainable inflation after decades of fighting deflation, and in anticipation of more sustainable growth following significant wage hikes from shunto collective bargaining negotiations, the BOJ ended yield curve control and its negative interest rate policy in March—shifting the policy rate from -0.1% to a range between 0% and 0.1%—and began scaling back on several of its quantitative easing purchase facilities for risk assets.4

The BOJ’s hawkish meeting on July 31 highlighted upside risks to inflation and a desire to gradually but steadily reduce monetary accommodation, sending markets into a deep albeit short-lived swoon. In addition to presenting a comprehensive plan for quantitative tightening through 2026, the BOJ increased its key rate to 0.25%, the highest level since 2008.5 It also intimated that further rate hikes were possible and could potentially exceed the 0.5% peak reached in the last hiking cycle preceding the global financial crisis.6

These hawkish moves from the BOJ are in contrast with dovish leanings from other central banks—especially repriced expectations for rate cuts from the Federal Reserve following a weak US jobs report shortly following the BOJ hike—and have narrowed the spread between policy rates. The resultant strengthening of the yen from generational lows triggered the unwinding of very overcrowded carry trades—in which investors borrow money in economies with low interest rates, such as Japan, to finance investments in higher-yielding markets—to the detriment of risk-assets worldwide.

Seeking to restore calm in the week following the turmoil unleashed by its July rate increase, BOJ Deputy Governor Shinichi Uchida issued dovish proclamations pledging to refrain from further rate hikes pending market stability. Investor anxiety was assuaged, and market expectations of a further 25 basis point hike this year fell from 60% immediately following the July 31 hike to 20%.7

Even with an uncertain timeline, further rate hikes seem likely, which could be problematic given Japan’s very high government debt (252% of GDP) and large fiscal deficit (5.8% of GDP).8 Given the massive amount of debt issued at ultra-low interest rates, however, Japan may have several years before higher contemporary rates meaningfully feed through to its interest expense. On paper, the Kishida government has targeted balanced primary fiscal accounts (which exclude interest payments) by FY2025 but has yet to specify plans. Moreover, the country hasn’t had a primary balance surplus since 1991.9 Over time, debt dynamics will become more problematic if the government is unable to consolidate its fiscal accounts amid higher interest rates.

While markets seem to have digested the BOJ’s initial steps toward normalization, at least for now, the sequence and magnitude of policy adjustments from here is key. Policymakers have a range of options—additional rate hikes, shrinking the BOJ balance sheet, enacting fiscal discipline or some combination thereof—but no easy answers. As discussed in the text box on page 6, the uncertain path forward has weighed on the yen.

... Corporate Governance Reform May Be a Source of Stability

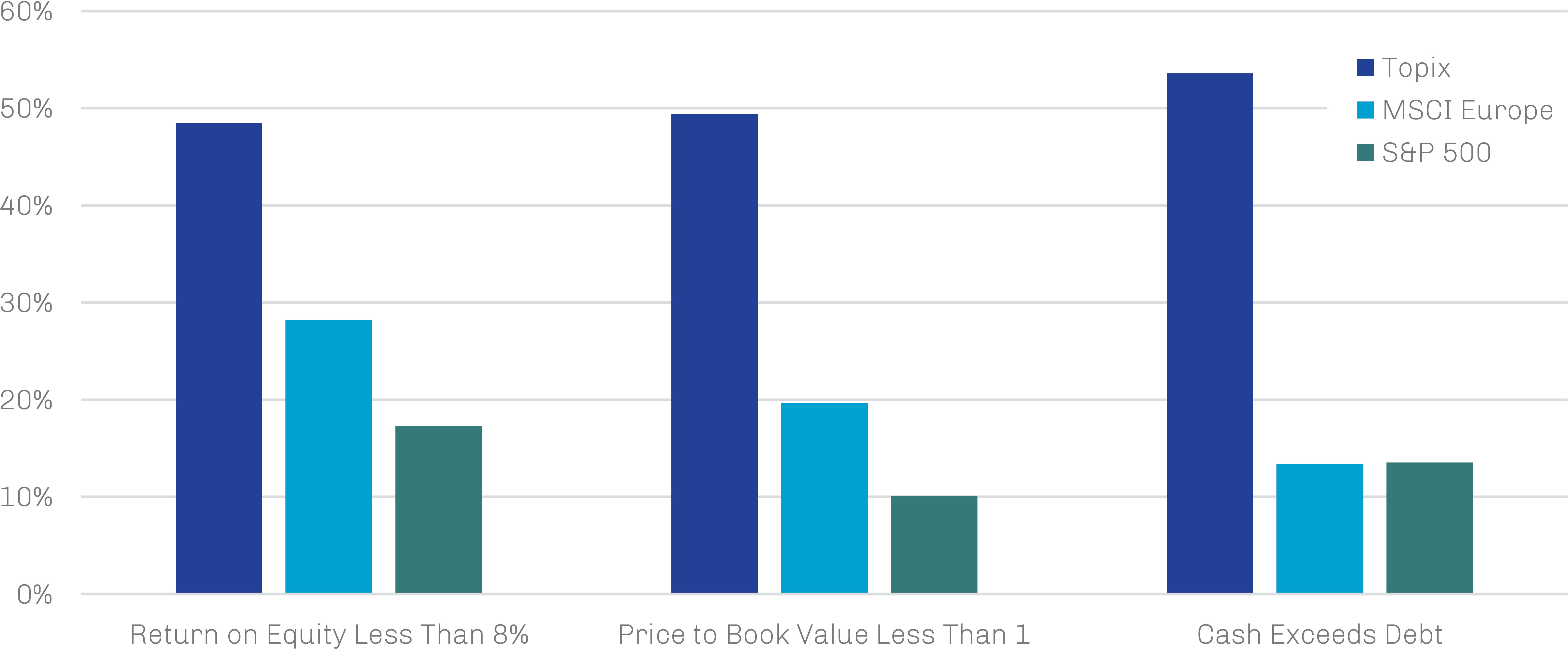

Even as certain supportive factors ebb and flow over time, improved corporate governance standards may provide long-term structural underpinnings to Japanese equities. For many years, activist investors clamored for improved capital allocation practices in Japan. More recently, the Tokyo Stock Exchange (TSE) itself has taken up the charge, advocating for enhanced shareholder returns. Specifically, updates to TSE’s Corporate Governance Code are designed to encourage Japanese companies to pursue sustainable growth strategies and prioritize improved capital allocation— including dividend increases, share buybacks and reduced cross-shareholdings—while encouraging the inclusion of independent directors on boards and improved engagement with investors (including disclosures in English).

These guidelines target the broad swath of listed companies believed to have untapped potential for profitability and growth, defined as those trading below book value or with returns on equity below 8%. As highlighted in Exhibit 2, approximately 50% of listings on the TSE meet these criteria. Given that more than 50% of Japanese companies also have cash balances that exceed debt,10 which often coincides with sub-standard returns and low valuations, ample runway may be available for additional dividend increases and share buybacks.

Exhibit 2. Japanese Companies Appear to Have Leeway to Improve Capital Allocation Practices…

Percentage of Companies Within Each Index Demonstrating Indicated Characteristic

Source: FactSet; data as of August 15, 2024.

Past performance is not indicative of future results.

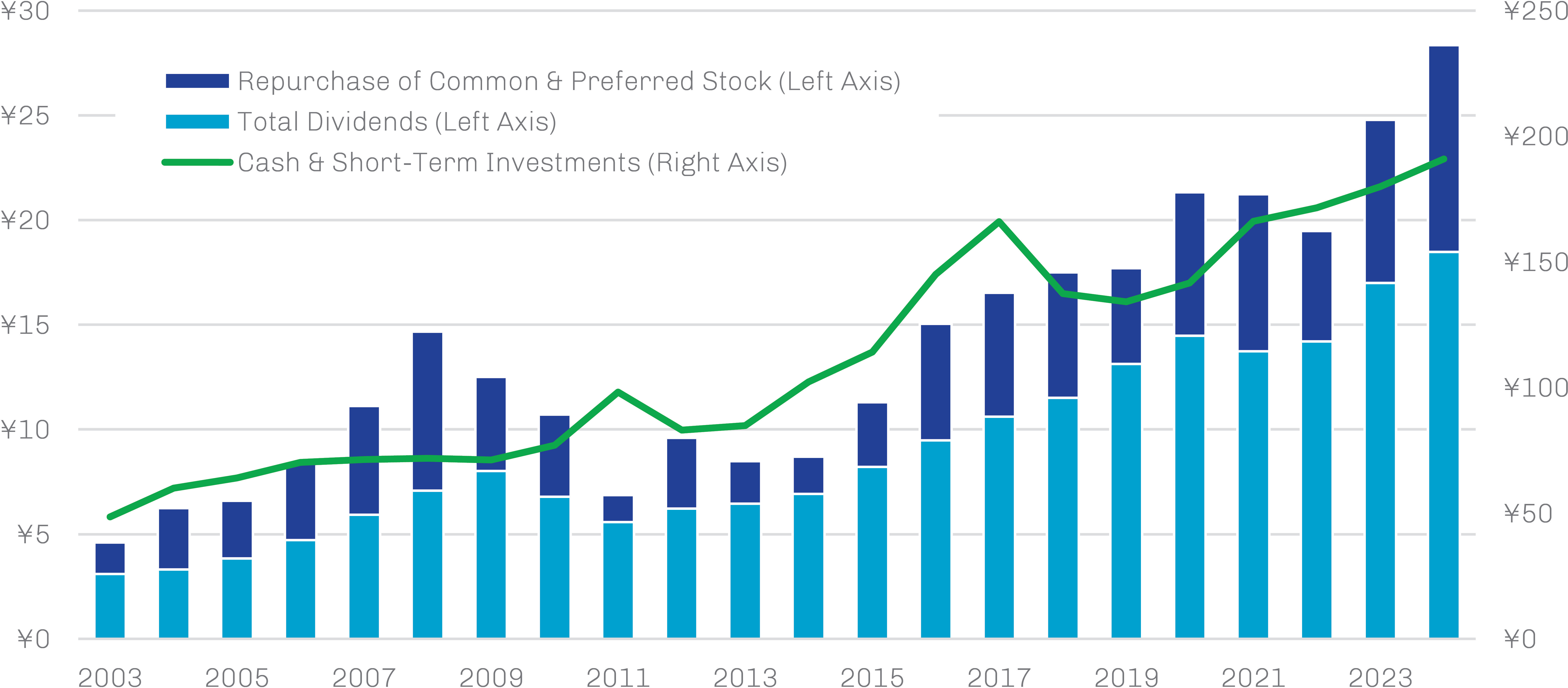

Perhaps triggered by TSE guidelines, the dash by managements to reduce cash by returning capital to shareholders is well underway, as shown in Exhibit 3. Yet despite increased dividends and share repurchases, cash continues to accumulate, suggesting many companies have further opportunity to reward shareholders.

Exhibit 3. …Especially Given Their Sizable Cash Hoards

Trillions of Yen, January 2002 through August 2024

Source: FactSet; data as of August 15, 2024.

Past performance is not indicative of future results.

Select Smaller Companies May Be Especially Attractive

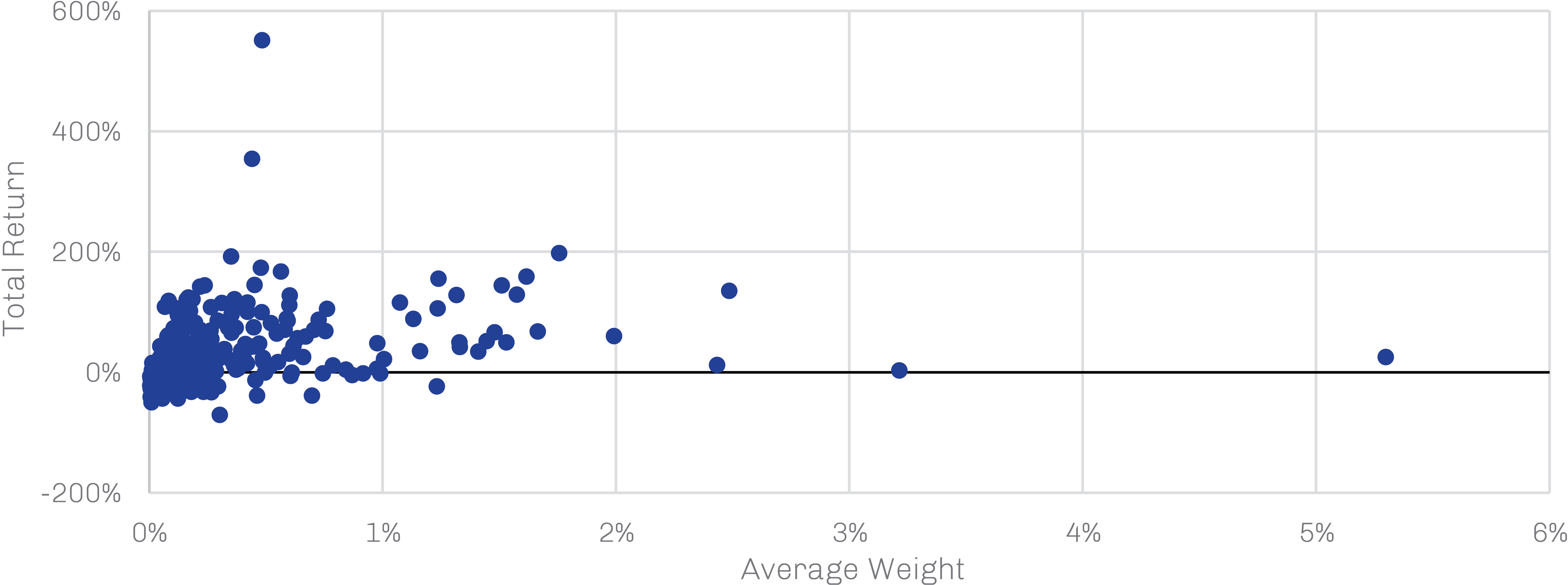

As investors the world over have continued to favor passive investment strategies, very large cap constituents of Japanese indexes have done especially well amid recent market strength. As shown in Exhibit 4, larger Japanese names historically have delivered uniformly positive performance, while greater dispersion is evident among those with smaller weightings in the index. In our view, this may suggest latent opportunity in a more eclectic group of companies whose qualities have yet to be fully recognized by the markets.

Exhibit 4. Large Index Constituents Have Led Gains in Japanese Equities

Total Return by Weight in the MSCI Japan Index, January 2023 through August 2024

Source: FactSet, MSCI; data as of August 15, 2024.

Past performance is not indicative of future results.

Within this investment universe, companies in structurally sound sectors may comprise an attractive opportunity set—specifically, companies that control long-duration real assets and have globally diversified sources of revenue rather than relying on Japan and its troubling demographics. Meanwhile, companies with durable cash flows across business cycles and strong or improving corporate governance practices may be of particular interest given their ability to tap into robust cash positions to improve shareholder value through dividend hikes, stock buybacks and the rationalization of operations. Such businesses can be found across a range of industries, including makers of bicycle components, commercial foodservice appliances and electronic equipment.

Seeking Stability and Resilience from the Bottom Up

Beyond its own ample idiosyncratic risk, Japan also faces many of the same challenges confronting the US and other Western nations. Global financial markets appear priced for moderate levels of risk aversion, and the emergence of an adverse economic development—if the US soft-landing scenario fails to play out, for example, or global sovereign debt concerns promote a broad repricing of government paper—could prompt a swift and significant reaction from markets. Additionally, the bifurcation between a de facto Eurasian heartland axis (North Korea, China, Russia and Iran) and the democratic alliance of countries on the globe’s periphery (the US, UK, Japan and Australia) could at best exert upward pressure on defense expenditures globally—and bring with it a continued broad upward thrust on budget deficits and rates. And should any one of the worldwide military hotspots ignite into a broader conflagration, more dire consequences could ensue.

While cognizant and sensitive to the short-run impact of macro and geopolitical factors on returns the world over, we believe that bottom-up stock picking—rooted in fundamental research—underpins portfolio resilience. With improved corporate governance as a structural bedrock, Japan, in our view, is an attractive destination for international diversification through selective exposure to high-quality, well-priced businesses.